- سبد خرید شما خالی است

- به خرید ادامه دهید

HDFC Ltd-HDFC Financial merger: What distinctions financial individuals should know just before progressing of MCLR to help you ELBR

- how to payday loan

- ارسال شده در

-

توسط سرزمین روغن

- 0 دیدگاه

ELBR is much more responsive to repo price transform, that can lead to smaller re also-cost regarding money versus MCLR

- Loans try linked with a standard rate, which is the reduced rates of which a lender can lend.

- Brand new MCLR try meant to guarantee that interest levels provided by banking companies moved quickly plus combination to your RBI’s repo rate actions.

- ELBR is more attentive to repo rate changes, that may lead to smaller re also-costs away from loans compared to MCLR.

The fresh new merger from HDFC Ltd having HDFC Bank has actually heralded good tall move in credit strategy to possess present home loan borrowers. Consequently, financial institutions have started transitioning consumers regarding the existing MCLR (Marginal Cost of Lending Speed) so you’re able to ELBR (Exterior Standard Credit Rate). That it move is key having borrowers understand, as you possibly can rather affect the equated monthly instalments (EMIs), the entire focus reduced, therefore the mortgage tenure.

Loans is associated with a standard rates, which is the reduced rates at which a lender is also lend. Banking institutions apply a credit spread-over so it standard. New pass on is decided based on products such as the borrower’s gender, revenue stream, credit rating, and loan amount. New standard plus the credit rating function the very last price regarding desire where that loan is offered.

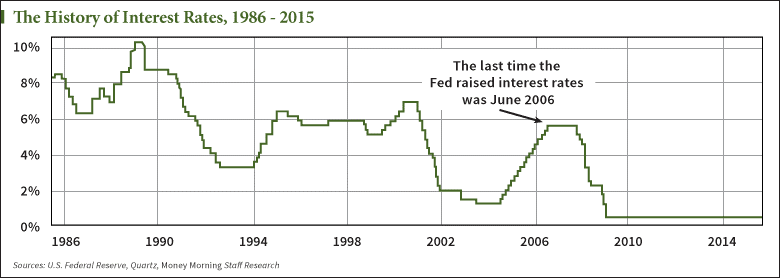

This new MCLR, delivered within the 2016 of the Set aside Lender out of Asia (RBI), are meant to make certain rates of interest offered by banking institutions moved easily plus tandem toward RBI’s repo price movements. However, so it financing rates design don’t achieve its pri, brand new RBI mandated all the finance companies to link its shopping mortgage costs in order to an external benchmark, like the repo rate, that is much more transparent and you can favorable so you can consumers.

HDFC Ltd-HDFC Financial merger: Exactly what differences mortgage individuals should become aware of ahead of moving forward from MCLR to help you ELBR

Adhil Shetty, President away from BankBazaar, claims, The brand new RBI put MCLR 7 in years past directly into change the Legs Speed system. MCLR is calculated because of the provided various circumstances, like the bank’s marginal price of funds, doing work can cost you, and you will statutory set-aside criteria. It reflected the cost of borrowing from the bank towards the bank and Nashville loans was supposed to be much more tuned in to alterations in this new wider financial criteria compared to the Foot Rates program. Financial institutions place their credit costs a variety of sorts of loans (mortgage brokers, personal loans, and business loans) adding a-spread otherwise margin along side MCLR. The latest give is determined according to the borrower’s borrowing chance, mortgage tenure, or other functional costs.”

An important factor to learn is the fact ELBR is far more receptive so you can repo speed alter, which can produce quicker re-prices from finance as compared to MCLR. Consequently one change in brand new repo rate usually now rating mirrored quicker in your EMIs significantly less than ELBR. Therefore, if the central lender incisions prices, the benefits often started to borrowers ultimately, and you will conversely, grows are passed away shorter.

EBLR is actually introduced to really make the alert of rate change much more clear, quick, and you will attentive to changes in the brand new wider discount getting users. In cases like this, mortgage loan is linked with an external benchmark speed as an alternative than just an internal speed lay by the lender in itself. This new RBI had during the 2019 delivered guidelines which need banks to link the financing pricing so you’re able to outside benchmarks such as the coverage repo speed set because of the main financial, the fresh new treasury expenses rates, or other field-computed rates,” told you Shetty.

Current HDFC home loan people might want to change to new ELBR program complimentary. not, borrowers must measure the positives and potential issues in advance of transitioning. The fresh new transparency and you can prompt changing nature away from ELBR might sound luring, but contemplate, shorter price news may increase the load inside a rising attention circumstance. Rather than for the MCLR, in which costs try reset all of the six otherwise one year, during the ELBR, changes in the latest repo speed impact the interest rates instantly.

Adopting the RBI required banking institutions in order to link financing pricing to EBLR, many banking companies transformed for the repo speed. The fresh repo speed noticed of a lot revisions – each other slices and nature hikes – introduced a modification of the new lending cost. Today, rate revisions been going on into the an even more predictable ways. Brand new MCLR, that has been foreseeable with regards to the durations away from rates news (particularly, immediately following from inside the half a year), try inside set by banking institutions and, therefore, more complicated to expect with regards to the quantum of your speed change. As well as, with old criteria, lenders don’t pass on the speed slices so you’re able to individuals from the exact same price while the price hikes. It occurrence out-of poor policy sign, that the RBI possess lamented usually, kept interest rates in the raised account.

“Which have EBLR home loans, price revisions was instantaneously passed on into the individuals. Just after dropping in order to 6.50 % prior to , home loans have increased to around 9 % as repo really stands within six.5 %. A reduced develops came down to step 1.90 per cent towards the eligible borrower, and so the low costs are now actually from the 8.forty percent range,” told you Shetty.

Very, should your home loan is related so you’re able to MCLR and you may feel paying a primary advanced over the industry rates. If that’s the case, you are able to envision using an EBLR once the spread over brand new repo price could have been falling, additional Shetty. New consumers are benefitting throughout the all the way down spread rate compared to current of these. Before generally making the newest switch, look at the give rate accessible to both you and do your maths knowing how much cash you will lay aside.

Shetty said, “While a prime borrower having a really high bequeath (dos.5-3 %), then it can be smart to refinance to a different repo-connected mortgage. The lower advances are fixed during the mortgage. When the rising prices try domesticated in the near future and also the repo rate falls, the latest prices perform immediately fall under 8% once again.”

If it’s reduced along with your interest is at level into brand new repo-linked financing, you will want to proceed with the MCLR system to avoid refinancing will set you back. In the event the, afterwards, interest levels slip, you could potentially relocate to a beneficial repo-linked mortgage to benefit about faster sign regarding speed incisions.

Thus, individuals is very carefully evaluate the newest financial situations, upcoming applicants or any other related facts before shifting regarding MCLR so you’re able to ELBR.